The Big Story

Q4 2022 is the best guide to the 2023 housing market

Quick Take:

- The 2023 housing market is poised to be more balanced between buyers and sellers than it has been over the past three years. Mortgage rates are softening demand, which has met the continued low supply of homes.

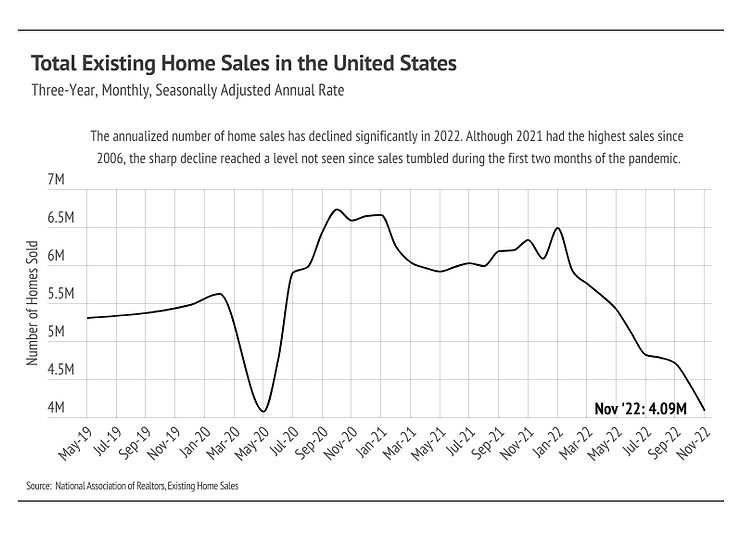

- Sales fell to levels not seen since the initial shock of the pandemic (April and May 2020). With fewer new listings and historically low inventory, sales likely won’t rebound to pre-pandemic levels.

- Inflation is slowly declining. If that trend continues, high mortgage rates may start to decrease in the second half of 2023.

Note: You can find the charts & graphs for the Big Story at the end of the following section.

A More Balanced Market in 2023

What happened yesterday has more bearing on today than what happened five years ago, so we’re shortening our lookback window to get a better understanding of what’s to come. This isn’t to say we can’t use history or that it should be dismissed entirely; rather, the pandemic set in motion a series of events that led to a different housing market, a different overall economy, and a different world when compared to pre-pandemic times. So, as many do in the new year, we reflect on the last year and envision what’s to come.

Major U.S. Housing Events 2020 - 2022

- Mid-March 2020 - May 2020: Concern over COVID-19 skyrocketed, leading to shelter-in-place orders across the United States and around the world. Seemingly everything shut down — including the real estate market because it’s very hard to buy or sell a home when you aren’t supposed to gather. By about the end of May 2020, it became clear that the virus wasn’t going away quickly, triggering the housing boom and the start of ultra-low mortgage rates.

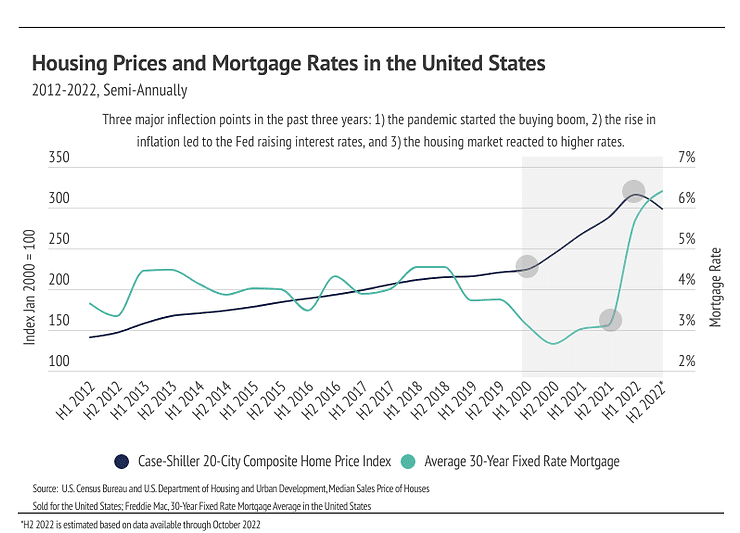

- June 2020 - December 2020: Asset prices, from housing to stocks to crypto to art, exploded due to a combination of easy money and a change in consumer behavior. The Federal Reserve lowered interest rates and poured money into the market, increasing the amount of money in circulation by 17% from February 2020 to May 2020. By the end of 2020, the money supply increased 24%, and by the end of 2021, it had risen 40%. Buyers were priced into the market as mortgage rates declined under 3% for the first time ever. Without a clear end to the pandemic in sight, buyers were incentivized to find a home they wanted to spend a lot of time in not only for rest, but also to work. With the increase in buyers, demand outstripped supply like we’ve never seen before. The number of homes for sale in the United States declined 34% in six months, while overall home prices increased 9%, according to the S&P/Case-Shiller 20-City Composite Home Price Index.

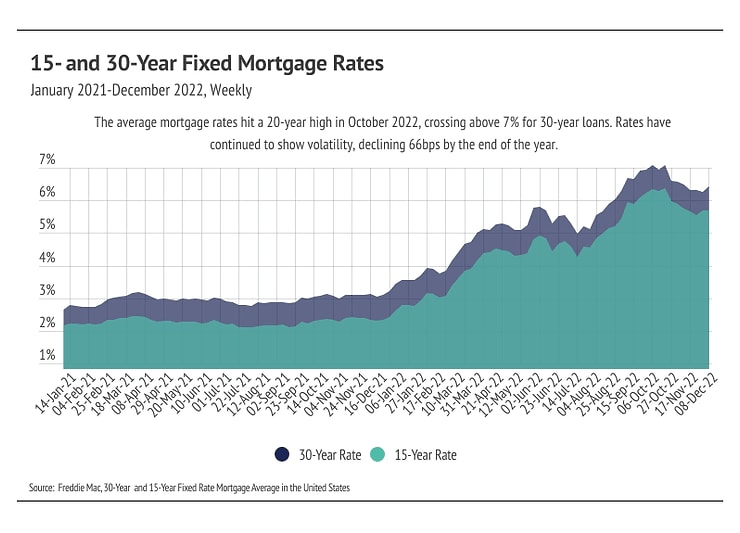

- January 2021 - December 2021: The year opened with the lowest 30-year average fixed mortgage rate on record: 2.65%. Mortgage rates hovered around 3% the entire year, with an average mortgage rate of 2.96% in 2021. The increase in buyers in the second half of 2020 was only a preview for 2021 sales, which were the highest since 2006. By the end of the year, home prices increased another 17% (29% in total since May 2020), and the number of homes for sale fell 52% since May 2020. Additionally, inflation rose quickly, and we closed the year with inflation at 7.09%, a level not seen since 1982. The Fed had one main tool to combat inflation: raising interest rates. Because the Fed said in December that it would begin raising rates in March 2022, it created the final buying boom as buyers and sellers rushed to the market to lock in low rates.

- January 2022 - June 2022: The last true sales spike occurred during the first quarter of 2022, which drove home prices up 5%. Sales began to slow, as did price growth. Home prices reached an all-time high in June 2022, increasing 42% since June 2020, which was the sharpest and quickest rise in home prices ever recorded. By the end of June, mortgage rates had risen 2.6% in 2022, which drastically decreased affordability.

- July 2022 - December 2022: During the second half of 2022, the housing market cooled significantly. Demand softened for several key reasons: higher interest rates, a return to seasonal market trends where prices increase in the first half of the year and decrease slightly in the second, and mean-reversion (about a million homes were sold above the average in 2021, and about a million fewer than the average were sold in 2022). We closed the year with high and volatile mortgage rates, hitting 20-year highs in October and November. The fourth quarter gives us a decent picture of what’s ahead.

2023 Outlook

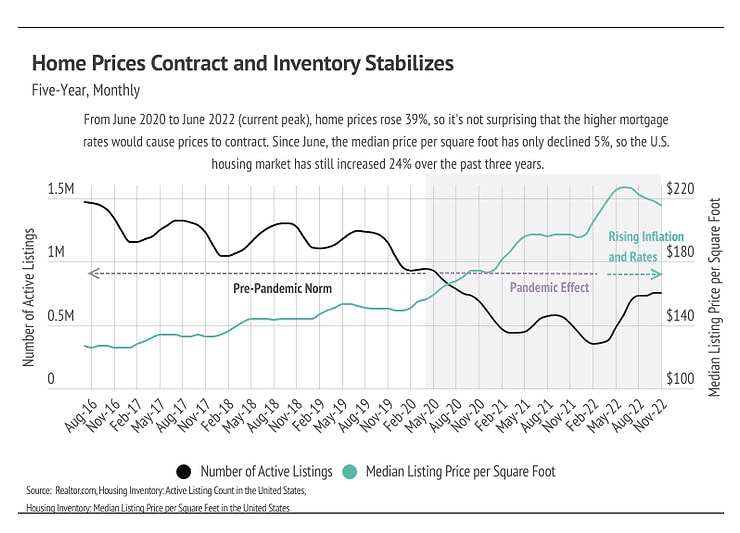

The economic factors are mixed, suggesting that the market is balancing out. Demand had nowhere to go but down after the rise in interest rates and the buying frenzy between 2020 and 2021. (The average homeowner stays in their home for about eight years.) The supply of homes is still about 20% below pre-pandemic levels, so the drop in demand brought the market closer to balance. In 2023, we expect a return to seasonal trends — price and inventory growth in the first half of the year and contraction in the back half — but at relatively lower levels, meaning fewer new listings and fewer sales overall.

The U.S. housing market has certainly shifted throughout the year, and we must recognize the current conditions homebuyers and sellers face. Of course, different regions vary from the broad national trends, so we’ve included a Local Lowdown below to provide you with in-depth coverage of your area. As always, we will continue to monitor the housing and economic markets to best guide you in buying or selling your home.

Big Story Data

The Local Lowdown

Quick Take:

- Although prices have contracted significantly, the East Bay housing market is entering 2023 as a sellers’ market, and we expect the market to remain favorable to sellers in the first half of the year.

- Home prices contracted into December 2022, which helped position prices to rise in the first half of 2023, as buyers and sellers adjust to higher mortgage rates.

- The housing market from 2020 to 2022 was an outlier, so it is adjusting back to more typical seasonal trends in 2023.

Note: You can find the charts/graphs for the Local Lowdown at the end of this section.

New Year, Old Normal

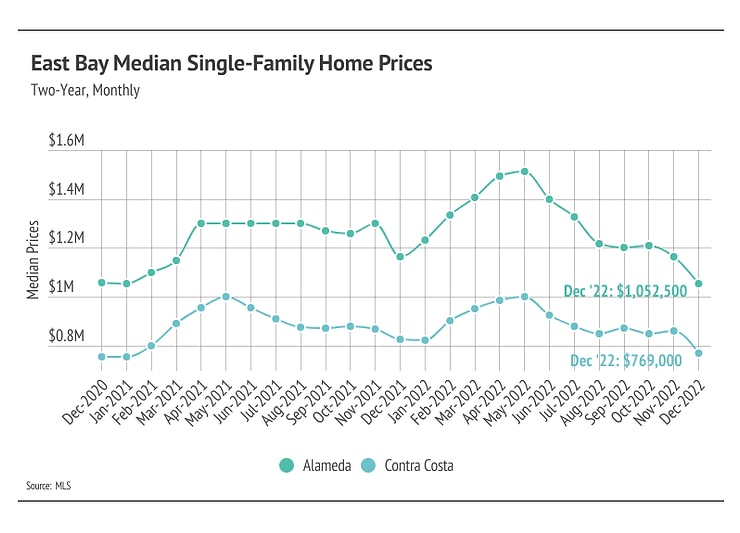

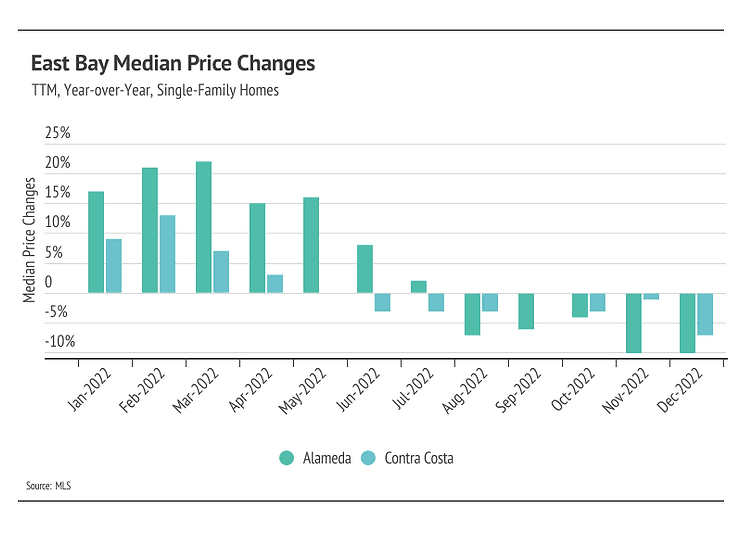

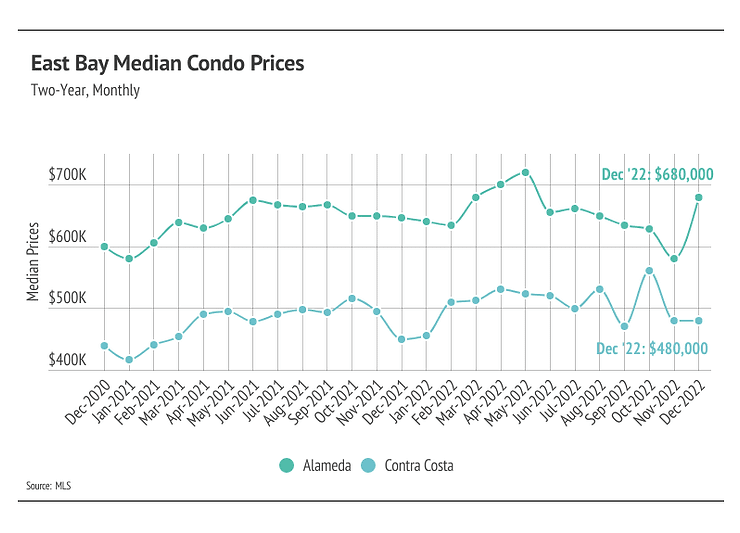

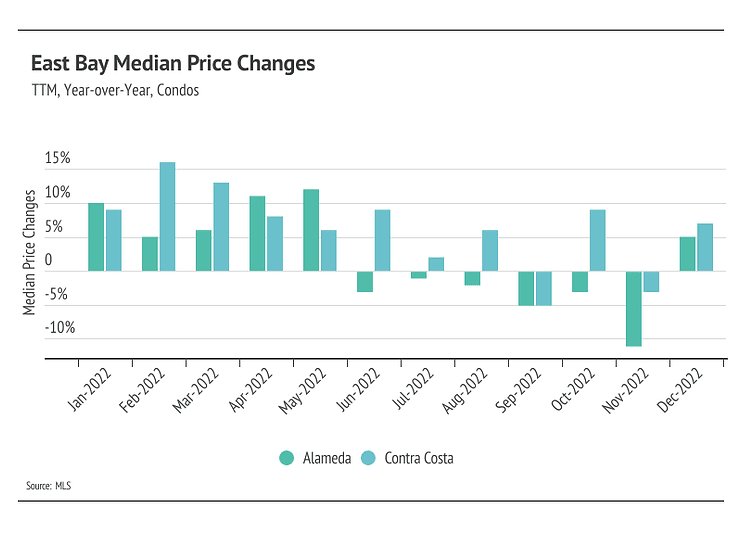

As we mentioned in the Big Story, the market has cooled for both buyers and sellers, largely because of higher interest rates. As we enter the new year, the market feels familiar — but from the era before 2020. Demand in the East Bay is evergreen, so we aren’t worried about matching buyers and sellers. That said, sellers likely won’t be getting multiple offers the second the home hits the market again anytime soon. To make a long story short, there is definitely less stress on the buying side of the market. Prices will most likely increase in 2023, but at a more modest rate of around 5-6%, which makes for a much healthier market than the volatile price movements that occurred over the past three years. Single-family home prices contracted in the second half of 2022, landing near 2020 prices in Alameda and Contra Costa, while condo prices have maintained some of their price gains. When we look back further to Q4 2019, single-family home prices have increased 27% in Alameda and Contra Costa, and condo prices have risen 10% in Alameda and 17% in Contra Costa. Without any signs of interest rates dropping, we’re entering a stage of slower, longer-term growth.

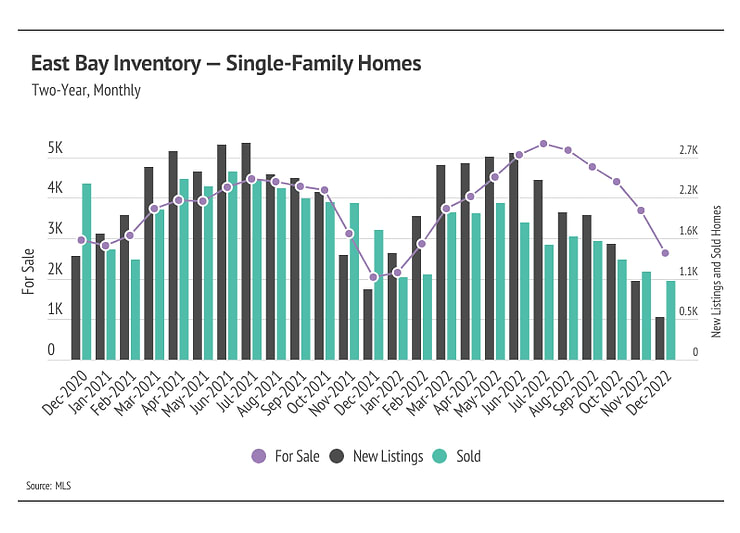

More New Listings Should Come to The Market in The First Quarter

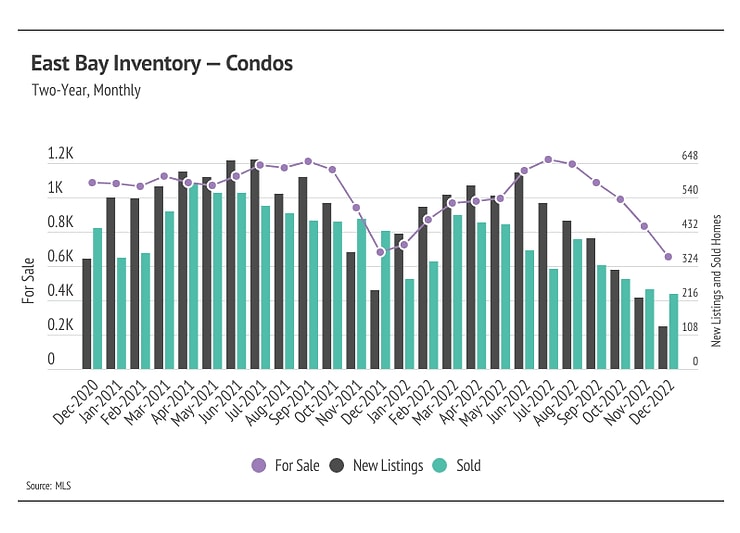

When we look at single-family home inventory levels for 2021 and 2022 side by side, the stark difference is immediately apparent. The 2021 market was defined by extremely high demand given the number of new listings, which kept inventory low throughout the year. In 2022, however, demand softened and the new listings far outpaced sales, allowing much-needed inventory to grow at a higher rate than the year before. In the second half of the year, fewer homes came to market and rising mortgage rates dropped demand, but supply fell faster, although inventory at the end of 2022 was higher than the all-time low in December 2021. The condo market had a simpler story in that there were fewer new listings without a proportional decline in sales, so inventory remained low, even reaching an all-time low in December 2022. This year, we expect the housing market to look a lot more like 2022 than 2021.

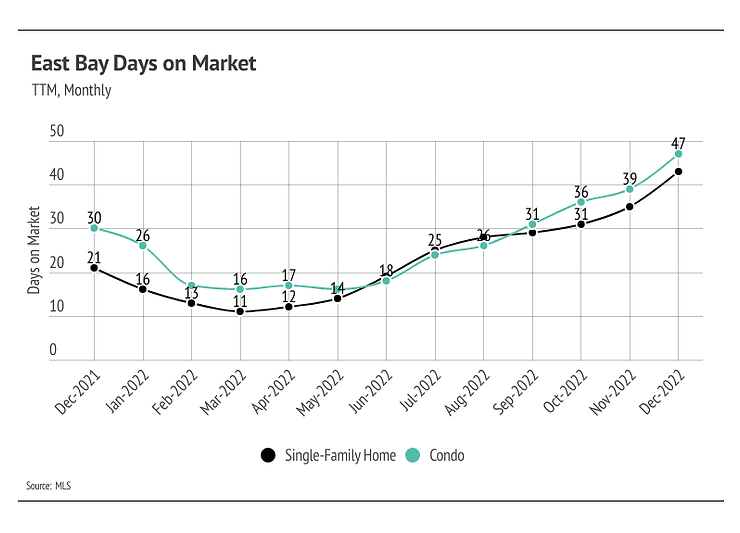

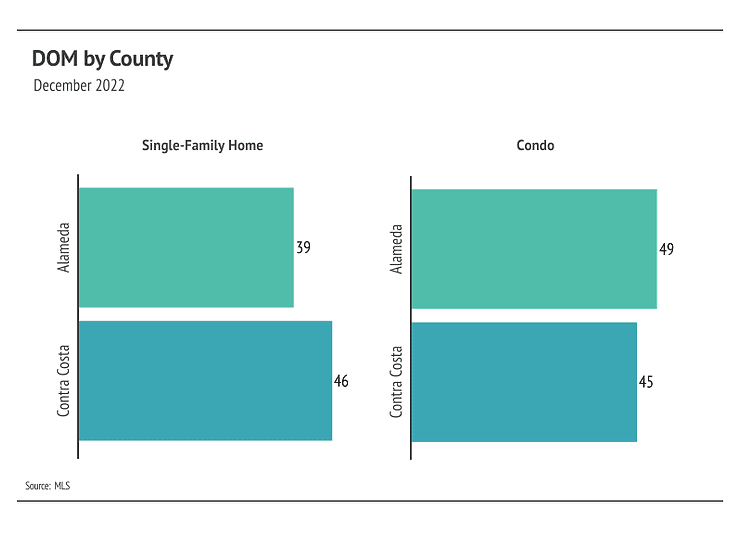

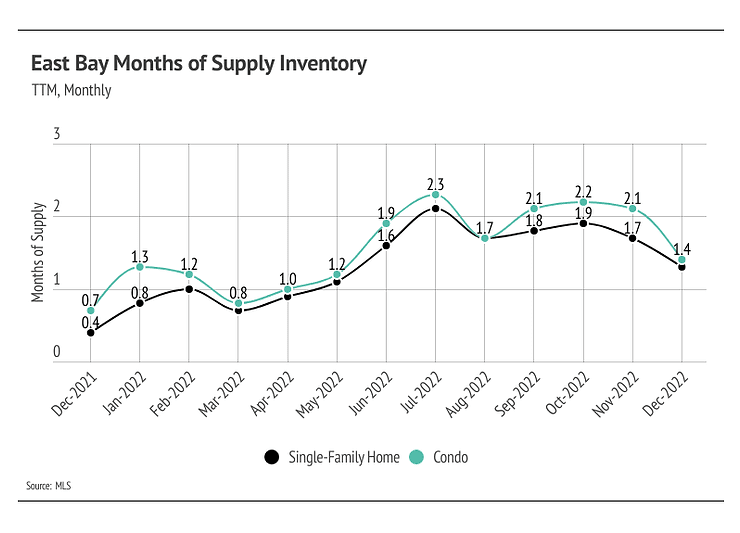

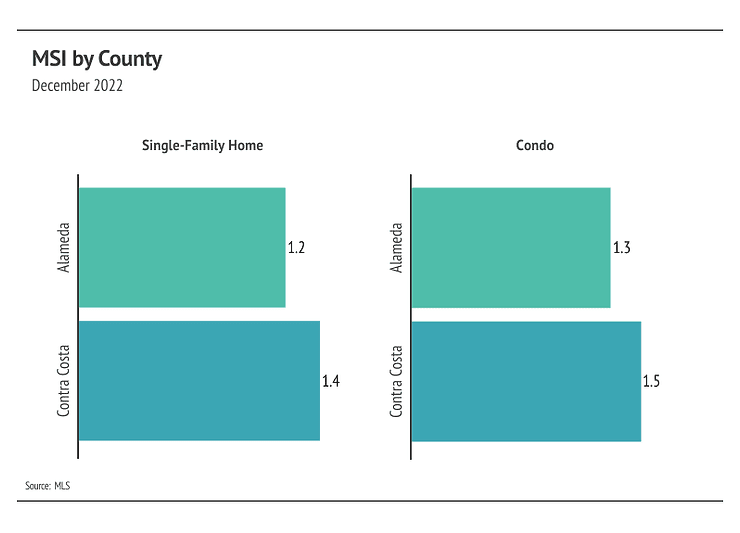

Months of Supply Inventory Implies a Sellers’ Market

Months of Supply Inventory (MSI) quantifies the supply/demand relationship by measuring how many months it would take for all current homes listed on the market to sell at the current rate of sales. The long-term average MSI is around three months in California, which indicates a balanced market. An MSI lower than three indicates that there are more buyers than sellers on the market (meaning it’s a sellers’ market), while a higher MSI indicates there are more sellers than buyers (meaning it’s a buyers’ market). MSI has trended higher since spring 2022 but leveled out near two months of supply before reversing, indicating the East Bay is still in a sellers’ market. Despite the changing economic environment, we are comfortable saying that the market will still favor sellers for at least the first quarter of 2023.

Local Lowdown Data